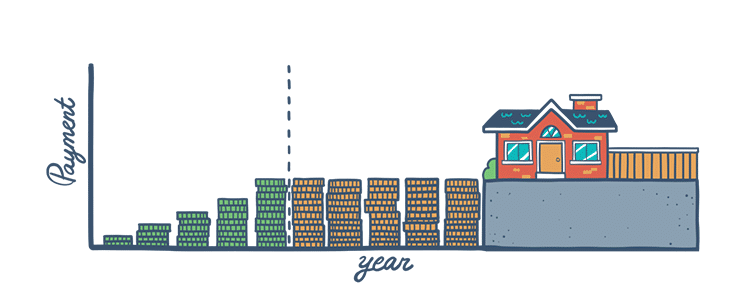

the homeowner owns minimal payments at the start of the mortgage

A graduated payment mortgage is designed in a way that the homeowner owns minimal payments at the start of the mortgage. The payment amount increases over time after the initial payment. This low initial interest rate qualifies the buyer for the loan, who otherwise wouldn’t be eligible. With a higher interest rate, and due to higher monthly payments, these buyers would be unable to qualify. This mortgage payment system is an especially attractive option for first-time or young homeowners whose income tends to rise gradually.

This type of mortgage may be used as a negative amortization loan if the accumulating interest amount is more than the initial payment. The borrower makes payments that are less than the interest charged on the note with this type of loan. Since payment structure postpones the interest payment, this causes the total principal of the loan to increase.

Only the Federal Housing Administration (FHA) issues loans with graduated payment mortgages. When approved, these loans allow low-to-moderate income borrowers to finance up to 96.5% of their home’s value, who otherwise wouldn’t be able to make such large down payment.

Higher total costs associated with the graduated-payment mortgage compared to a traditional mortgage are its main disadvantage. As the interest rates and payments go up, the borrowers may realize that they are not reducing the principal borrowed and are only paying the interest.

The borrower will pay even more interest if the graduated payment mortgage is a negative amortization loan. The total principal of the loan rises as the postponed interest payment adds to its overall value.

With increased mortgage payments, there is no guarantee that the borrower’s income will increase as well. This should be taken into consideration, since failing to pay the loan will damage the borrower’s credit and allow the lender to foreclose the property.

Experts at Champions Mortgage took some time and made a quick step by step loan guide that will help you understand it better. However, if at any moment you feel confused or need further explanation, don’t hesitate to call us.

Champion Mortgage professionals will gladly guide you through every step of the way.