Champions Mortgage helps Texas homebuyers and homeowners secure conventional loans the most common type of mortgage in the United States, not backed by a government agency. Conventional loans in Texas

offer 3% down payment options, competitive interest rates for borrowers with strong credit, and no upfront mortgage insurance. As a mortgage broker with access to 50+ wholesale lenders, we find the most

competitive conventional loan rate for your credit profile and close most loans in 21 days.

Conventional Loans offer a variety of benefits that make them an excellent choice for many borrowers:

For Texas homebuyers with strong credit, a 3% down conventional loan

costs less over time than a 3.5% FHA loan because conventional loans

do not carry life-of-loan mortgage insurance.

Conventional loan rates are typically lower for borrowers with a credit score of 740 or above. The 620 minimum qualifies you to apply but raising your score to 740 before applying can meaningfully reduce your

rate and monthly payment over the life of the loan. Champions Mortgage compares conventional rates across 50+ wholesale lenders to find the lowest available rate for your profile.

Choose from fixed-rate conventional loans (such as 15-year or 30-year terms) or adjustable-rate mortgages (ARMs) to suit your financial goals.

Conventional loan limits are set annually by the Federal Housing Finance Agency (FHFA) based on Fannie Mae and Freddie Mac guidelines. For 2026,

the conforming loan limit for most Texas counties is $[verify at FHFA.gov. Loans above this limit are nonconforming — also called jumbo loans —

and carry different rate and qualification requirements.

FHA loans charge a 1.75% upfront mortgage insurance premium at closing.

Conventional loans skip this entirely — saving Texas buyers $3,500 to $7,000+ on a typical home purchase depending on loan amount.

Conventional loans also allow PMI to be cancelled automatically once your loan balance reaches 78% of the original purchase price — under the federal Homeowners Protection Act. You can also request cancellation at 80% LTV. FHA loans with less than 10% down require mortgage insurance for the life of the loan with no automatic cancellation.

A conventional loan is a mortgage not backed or insured by any federal government agency — unlike FHA loans (Federal Housing Administration), VA loans (Department of Veterans Affairs), or USDA loans (U.S Department of Agriculture). Because there is no government guarantee, conventional lenders typically require higher credit scores and stricter qualification standards.

Conforming loans: Meet the loan limit and underwriting guidelines set by Fannie Mae and Freddie Mac — the two government-sponsored enterprises that purchase and securitize most conventional mortgages in the United States. The 2026 conforming loan limit for most Texas counties is $ [verify at FHFA.gov before publishing]. Conforming loans are the most

common type of conventional loan and typically carry the most competitive interest rates.

Exceed the conforming limit or do not meet Fannie Mae or Freddie Mac underwriting standards. Jumbo loans — conventional

mortgages above the conforming limit — fall into this category. Nonconforming loans carry different qualification requirements and rate structures. Texas homebuyers purchasing within the conforming limit benefit from

the widest range of lender competition and the lowest conventional mortgage rates available.

To be eligible for a conventional home loan, borrowers typically need:

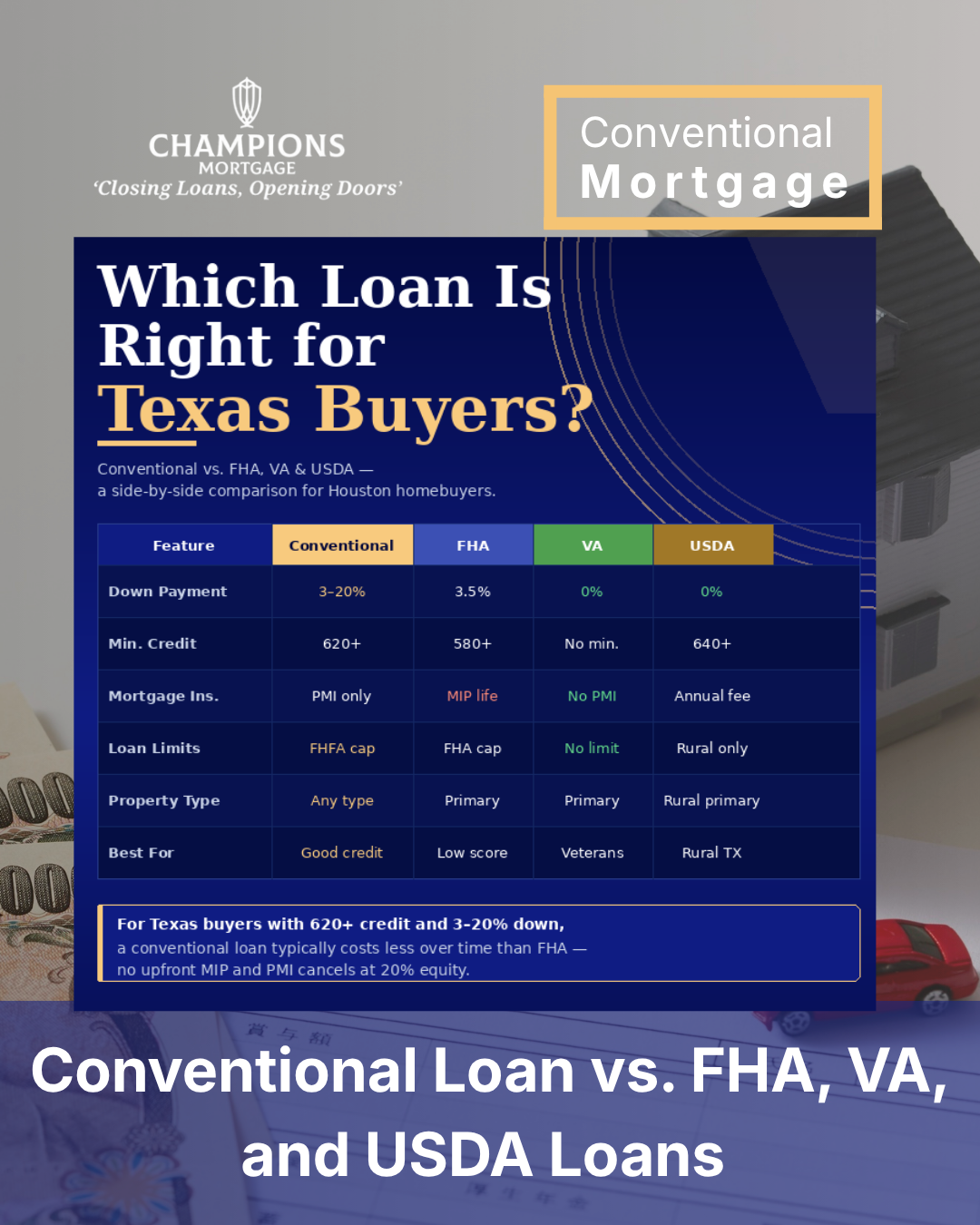

Conventional loans are the most common mortgage choice for Texas buyers

with strong credit and a down payment. Here’s how they compare to

government-backed alternatives:

Conventional vs. FHA: FHA loans require only 580 credit score and 3.5%

down but carry a 1.75% upfront MIP and life-of-loan mortgage insurance

for most borrowers. Conventional loans avoid upfront MIP entirely and

allow PMI cancellation at 20% equity. For Texas buyers with a 620+

credit score, a conventional loan typically costs less over time than

an FHA loan.

Conventional vs. VA: VA loans offer zero down payment and no PMI for

eligible veterans — making them the strongest benefit available to

qualifying military borrowers in Texas. Non-veterans and borrowers who

have exhausted their VA entitlement use conventional financing instead.

Conventional vs. USDA: USDA loans offer zero down payment for buyers

purchasing in eligible rural Texas areas. They carry an upfront guarantee

fee and annual fee similar to FHA MIP. Conventional loans are used for

purchases in areas where USDA eligibility does not apply — including

most Houston, Dallas, and urban Texas markets.

If you have a 620+ credit score and a 3% down payment, a conventional

loan in Texas is likely the most cost-effective option. A Champions

Mortgage loan officer compares all programs available for your situation

before you apply.

When you choose Champions Mortgage, you benefit from:

Our loan officers handle conventional loan applications across Texas daily. We know Fannie Mae and Freddie Mac underwriting requirements, which conforming programs accept 3% down, and how to structure your loan to avoid PMI without a 20% down payment.

As a mortgage broker with access to 50+ wholesale conventional lenders, Champions Mortgage compares rates across multiple investors for each Texas borrower. The rate difference between lenders on a 30-year conventional loan can total tens of thousands of dollars over the life of the loan.

Most Champions Mortgage conventional loan applications close in 21 days. 96% of our applicants close with us. We identify required documentation upfront — W-2s, tax returns, pay stubs, and bank statements — so underwriting does not create last-minute requests.

We compare conventional purchase loans, conventional refinances, and cash-out refinances to find the right fit for each Texas borrower. If a different program — VA, FHA, or USDA — serves your situation

better than conventional financing, we say so upfront.

4.9-star Google rating from Houston homebuyers. Real loan officers answer your calls. We explain conventional loan estimates, appraisal results, and underwriting conditions in plain language — no jargon.

Start by filling out our easy online mortgage application, and our team will review your eligibility.

We help you compare conventional mortgage rates to find the most competitive option.

Provide documentation of your income, assets, and credit to finalize your loan approval.

Once your loan is approved, you can close quickly and move into your new home!

Hear from our satisfied clients who have used conventional mortgages to achieve their homeownership dreams:

Most Texas conventional lenders require a minimum credit score of 620. However, the best conventional loan rates in Texas are typically reserved

for borrowers with scores of 740 or above. Raising your score before

applying — by paying down credit card balances and avoiding new credit

inquiries — can meaningfully reduce your monthly payment over a 30-year

loan term.

Conventional loans allow down payments as low as 3% for first-time

homebuyers and 5% for most other borrowers. A 20% down payment eliminates

private mortgage insurance entirely. Between 3% and 20%, you pay PMI

until your loan balance reaches 80% of your home's value — at which

point you can request cancellation. PMI cancels automatically at 78%

LTV under the Homeowners Protection Act.

Conventional loans require private mortgage insurance (PMI) when your

down payment is less than 20%. PMI rates typically range from 0.5% to

1.5% of your loan amount annually. Unlike FHA mortgage insurance, PMI

on a conventional loan can be cancelled — either by request at 80% LTV

or automatically at 78% LTV under the Homeowners Protection Act. This

is a key advantage over FHA loans, where mortgage insurance remains

for the life of the loan for most borrowers.

Yes! Conventional loans are ideal for investment properties and second homes.

Conventional loans require a minimum credit score of 620. Borrowers

with scores below 620 may qualify for FHA financing (580 minimum with

3.5% down) or VA loans (no set minimum for eligible veterans). If your

score is between 580 and 619, working with a Champions loan officer

to review all available programs is the best starting point before

applying anywhere.

If you’re ready to buy a home with a conventional loan, secure competitive mortgage rates, or refinance your existing loan, Champions Mortgage is here to help!

At Champions Mortgage, we are committed to helping you find the best home financing solution. Contact us today and start your conventional loan application with a trusted mortgage partner!