Right now, buying a home means facing mortgage rates that are a world away from the historic lows buyers locked in between 2019 and 2022. For many buyers, that gap between then and now translates to hundreds of extra dollars every single month. But there is a financing strategy that lets you sidestep today’s elevated rates entirely — and it’s called an assumable mortgage.

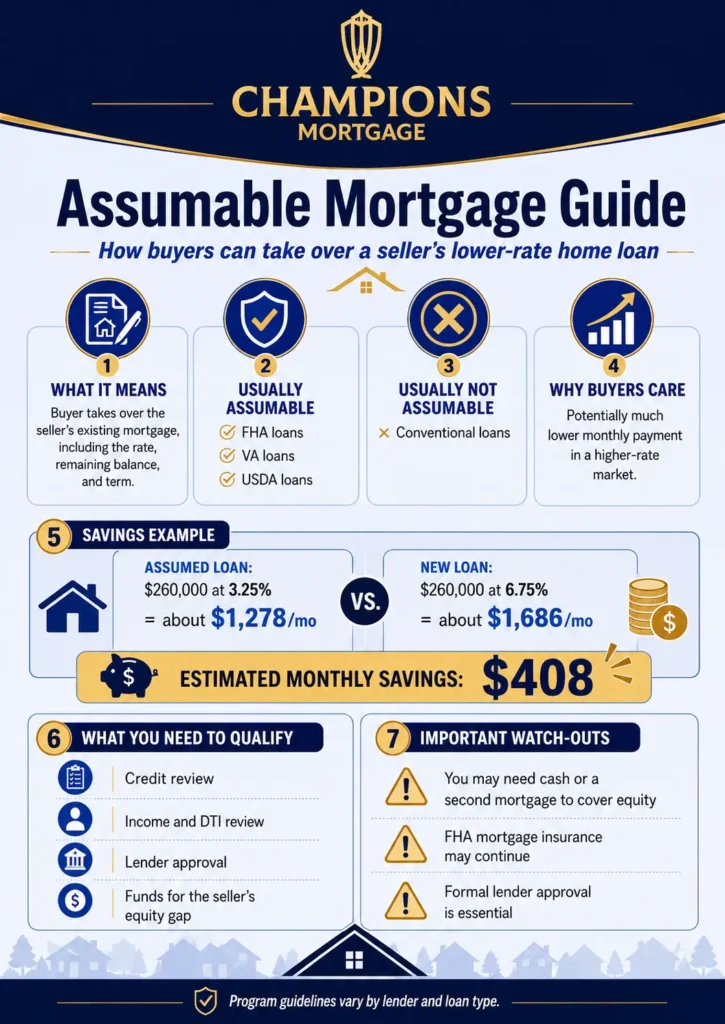

An assumable mortgage loan allows a buyer to step into the seller’s existing mortgage and keep the original interest rate, remaining balance, and repayment terms intact. If that seller locked in a rate of 3.25% back when rates were at historic lows, you — as the buyer — can assume that mortgage and make payments at that same lower rate, not the 6% or 7% rate the market currently offers.

This guide breaks down exactly how an assumable mortgage works, which types of home loans are assumable, how to qualify, what it costs, and whether it’s the right move for your situation. If you’re buying a home in today’s rate environment, this is a strategy worth understanding inside and out.

| Key Takeaways An assumable mortgage lets a buyer take over the seller’s existing home loan — including the original interest rate.FHA loans, VA loans, and USDA loans are generally assumable. Conventional mortgages are typically not assumable.Buyers can save hundreds of dollars per month by assuming a lower-rate mortgage.You must qualify with the lender — credit score, DTI, and income are all reviewed.The buyer must cover the seller’s equity via cash or a second mortgage.Approximately 12 million active assumable mortgages exist in the US today. |

What Is an Assumable Mortgage?

An assumable mortgage is a type of home loan that can be transferred from the current homeowner to a new buyer. Instead of applying for a brand-new mortgage, the buyer takes over the seller’s existing mortgage — including the remaining loan balance, the original interest rate, and the remaining repayment period.

Think of it this way: the seller locked in a rate years ago when mortgage rates were low. By assuming that loan, you inherit their rate rather than accepting whatever today’s market offers. The mortgage contract transfers to you, and you become responsible for making all future payments on the mortgage.

The concept has been around for decades, but it becomes especially valuable during periods of rising interest rates — exactly the environment many homebuyers face today. According to Home Mortgage Disclosure Act data, roughly 32% of mortgages originated in recent years are government-backed and potentially assumable, representing an estimated 12 million active assumable mortgages across the country.

| Expert Tip Search for homes listed as ‘assumable mortgage’ or ask your loan officer to identify FHA, VA, or USDA listings in your target area. Assumable mortgage listings are becoming a competitive differentiator for sellers in high-rate environments. |

How Does an Assumable Mortgage Work?

The mechanics of assumable loans are straightforward, but there’s one critical piece of math that trips people up: the home equity gap.

Here’s the situation: suppose the home you want to buy is valued at $400,000. The seller’s remaining mortgage balance is $260,000. If you assume the mortgage, you take over a loan with a $260,000 balance. But the seller has $140,000 in equity built up in the home that they need to be compensated for. That difference — the equity gap — must come from somewhere.

You have two options to cover the equity difference: pay it in cash at closing, or take out a second mortgage to finance it. That second mortgage will typically carry a higher interest rate than the assumed loan, but the savings on the primary balance usually more than offset it.

Two Types of Mortgage Assumption

Novation-based assumption: This is the standard approach for government-backed loans. The lender is fully involved, reviews the buyer’s credit and income, and — once approved — formally releases the seller from liability. This is the cleanest and safest route for both parties.

Simple assumption: The buyer and seller privately agree to transfer the mortgage obligation without formal lender involvement. This is riskier: the seller often remains on the hook if the buyer defaults. Some older FHA loans originated before December 1986 allowed simple assumption, but they are increasingly rare.

What Happens to the Seller?

The seller’s outcome depends entirely on how the mortgage assumption process is handled. With a proper novation-based assumption, the lender issues a release of liability, and the seller walks away with no further obligation on that mortgage. Without formal lender approval, the seller’s credit remains at risk if the buyer stops making payments. Always go through the official lender channel.

Real-Dollar Savings: Assumed vs. New Mortgage

Here’s a side-by-side look at what assuming a lower-rate loan actually means for your monthly budget:

| Scenario | Assumable Mortgage | New Mortgage |

| Assumed loan balance | $260,000 | $260,000 |

| Interest rate | 3.25% (assumed) | 6.75% (new loan) |

| Monthly P&I payment | $1,278 | $1,686 |

| Monthly savings | $408/month | — |

| Annual savings | $4,896/year | — |

| Savings over remaining term | $107,000+ | — |

* Example based on a $260,000 balance, 22 years remaining. Actual savings vary by loan balance and rate differential.

Types of Assumable Mortgages

Mortgages are assumable when they are backed by a federal government agency. Here’s a breakdown of each loan type that allows assumption, including what to expect from each program.

FHA Assumable Mortgage

Every loan insured by the Federal Housing Administration (FHA) is assumable. FHA loan assumption is one of the most common types because FHA loans are widely used by first-time buyers and don’t include the due-on-sale clause that conventional mortgages carry.

FHA loan assumption requirements:

- Minimum credit score: 580 (some lenders require 620)

- Debt-to-income ratio (DTI) of 43% or less

- Proof of income and employment

- The seller must have used the property as their primary residence

- Lender creditworthiness review must be completed within 45 days

One important cost to note: FHA mortgage insurance premium (MIP) transfers with the loan. The annual MIP — typically between 0.55% and 1.05% of the loan balance — continues for the life of the loan. However, you won’t pay the upfront MIP of 1.75% again, since the original borrower already paid it. On a $260,000 loan, that’s roughly $4,550 you don’t owe at closing.

For a deeper look at FHA eligibility and programs, see the Champions Mortgage FHA Home Loans page.

VA Assumable Mortgage

Loans guaranteed by the Department of Veterans Affairs are also assumable, and here’s a detail that surprises many buyers: non-veterans can assume a VA loan. You don’t need to be a veteran or active-duty military member to qualify. You do need to meet the lender’s credit and income standards, and both the VA and the mortgage servicer must approve the transfer.

If a non-veteran assumes the loan, the selling veteran’s VA loan entitlement stays tied to that mortgage until it’s fully paid off, which can limit their ability to use VA benefits on a future purchase. If a veteran buyer with their own entitlement assumes the loan, they can substitute their entitlement and free up the seller’s.

VA assumption fee: The VA charges a funding fee of 0.5% of the remaining loan balance on assumptions. On a $250,000 balance, that’s $1,250 — far less than the cost of originating a new loan.

VA loan assumptions surged over 700% between 2021 and 2023 as buyers rushed to secure below-market rates. To understand the full range of VA loan benefits, visit the VA Loans of Champions Mortgage .

USDA Assumable Mortgage

USDA loans — designed for properties in eligible rural areas — are also assumable, though with a narrower pool of qualified buyers. The buyer must meet the USDA’s income eligibility standards, which generally require household income to be at or below 115% of the area median income. The property must remain in a USDA-eligible location, and the current owner must be current on their payments.

The USDA charges a guarantee fee of 1% upfront and an annual fee of 0.35% of the remaining loan balance. Processing fees for USDA assumptions typically run between $300 and $500.

Conventional Mortgage: Typically Not Assumable

Here’s the short answer: conventional mortgages cannot be assumed in most cases. Most conventional loan contracts contain a due-on-sale clause that requires the full mortgage balance to be repaid when ownership transfers. This clause exists to protect the lender from inheriting a borrower they didn’t vet.

There is one narrow exception: some adjustable-rate mortgages (ARMs) under conventional programs may allow assumption, depending on the specific loan contract. But this is uncommon, and the rate adjusts periodically, so the savings aren’t the same as with a fixed-rate government loan.

Assumable Mortgage Loan Types at a Glance

Use this table to compare the key features of each assumable loan type:

| Feature | FHA Loan | VA Loan | USDA Loan |

| Assumable? | Yes | Yes | Yes |

| Min. Credit Score | 580 | No VA minimum* | 640 (typical) |

| Max DTI | 43% | 41% (guideline) | 41% |

| Assumption Fee | Varies | 0.5% of balance | $300–$500 |

| Non-veteran eligible? | N/A | Yes | Must meet USDA income limits |

| MIP/Fee Transfer? | Yes (annual MIP) | VA funding fee applies | Annual fee 0.35% |

| Approval Timeline | 45 days | 45 days | Varies |

* VA does not set a minimum FICO score but lenders may have overlays. The VA prohibits overlays beyond its guidelines.

How to Qualify for an Assumable Mortgage

Qualifying for an assumable mortgage works similarly to qualifying for a new home loan. The lender will review your financial profile to determine whether you can take on the mortgage loan responsibly. Here’s what they look at:

Credit Score Requirements

Your credit score is one of the first things any lender checks. For FHA assumptions, most lenders require a minimum credit score of 580, though some set the threshold at 620. VA and USDA assumptions don’t have a fixed federal floor, but individual lenders typically require a score in the 620–640 range. The good news: your score doesn’t need to match what the original borrower had — it just needs to meet today’s minimum.

Debt-to-Income Ratio (DTI)

Your debt-to-income ratio measures your total monthly debt payments against your gross monthly income. For FHA assumptions, the maximum DTI is typically 43%. VA guidelines suggest 41%, though compensating factors can allow higher ratios. Lenders want to confirm that your income is sufficient to support the assumed monthly mortgage payment plus any other existing obligations.

Down Payment and Equity Gap

This is the most common sticking point when considering an assumable mortgage. You must cover the difference between the mortgage balance and the home’s current value — the seller’s equity. Options include:

- Pay the equity gap in cash at closing

- Take out a second mortgage (typically at a higher rate than the assumed loan)

- Negotiate with the seller on the sale price to reduce the equity gap

Documentation Required

- Proof of income (W-2s, tax returns, or bank statements)

- Recent pay stubs

- Verification of assets for the down payment

- Credit report authorization

- Mortgage pre-approval or lender application (for the second mortgage, if applicable)

| Common Mistake to Avoid Don’t skip the formal lender approval process for a mortgage assumption. A simple assumption made without lender involvement leaves the seller liable if you default on the loan — and can expose you to legal complications if the lender invokes the due-on-sale clause. |

Assumable Mortgage Pros and Cons

Every financing strategy has trade-offs. Here’s an honest breakdown of what works in your favor — and what to watch out for — when assuming a mortgage:

| ✅ Pros for the Buyer | ⚠️ Cons to Consider |

| Lock in a below-market interest rate — potentially 2–4% lower than today’s rates | Large down payment or second mortgage required to cover the seller’s equity |

| Lower monthly mortgage payments compared to a new mortgage | Second mortgage to cover the equity gap typically carries a higher interest rate |

| Reduced closing costs — many fees are capped on assumable loans | FHA MIP transfers and lasts the life of the loan |

| No appraisal required in most cases | VA entitlement may not be restored if a non-veteran buyer assumes the loan |

| Faster equity building — you’re not resetting to a 30-year clock | Lengthy approval process — can take 45–90 days |

| No upfront MIP on FHA assumption (original borrower already paid it) | Seller remains liable if buyer defaults and lender approval isn’t obtained |

For Sellers: Why It Matters

Sellers with assumable loans can use them as a competitive advantage. In a market where buyers are rate-sensitive, listing a property with an assumable mortgage at 3.25% attracts more buyers, can support a higher sale price, and often makes the property easier to sell than comparable homes without this feature.

The main risk for sellers: if the assumption isn’t handled through proper lender channels, they remain on the hook for the mortgage even after ownership transfers. Always obtain a formal release of liability before completing the sale.

Cost to Assume a Mortgage: What to Budget

One of the biggest advantages of an assumable loan is that the closing costs are typically lower than those on a new mortgage. Many loan origination fees and underwriting costs are capped or waived in assumptions. Here’s what to plan for:

- Assumption fee: Charged by the lender; varies by loan type. VA: 0.5% of balance. FHA/USDA: typically $500–$1,000 or capped by program guidelines.

- Title transfer fee: Standard closing cost for transferring property ownership.

- VA funding fee: 0.5% of the remaining loan balance for VA assumptions.

- USDA processing fee: $300–$500 for USDA loan assumptions.

- FHA ongoing MIP: The annual mortgage insurance premium transfers to you and continues for the life of the loan.

- Second mortgage costs: If you’re financing the equity gap, you’ll pay standard origination fees and closing costs on the second loan.

The combined cost of an assumption is almost always lower than the expense of a new mortgage origination — especially when you factor in the ongoing savings from the lower interest rate.

How to Find Mortgage Assumable

Not every listing advertises its loan type, so you’ll need to be proactive to find an assumable mortgage. Here are the most effective approaches:

- Ask your real estate agent to filter for FHA, VA, or USDA listings in your target area.

- Check assumable mortgage listing platforms like AssumeList or Roam, which specialize in surfacing homes with assumable loans.

- When you identify a home you like, ask the seller’s agent directly: ‘Is the current loan FHA, VA, or USDA? Is it assumable?’

- Work with an experienced mortgage lender who understands the assumption process and can verify loan eligibility before you make an offer.

- Near military installations, VA loan concentrations are high — a strong market for VA assumptions.

The Champions Mortgage team regularly works with buyers to identify assumable mortgage listings and navigate the assumption process in Texas. Whether you’re looking at a VA loan assumption, an FHA assumption, or exploring other home purchase loan options, we can walk you through every step.

Considering an Assumable Mortgage is Right for You?

An assumable mortgage could be a smart move if the following conditions apply to your situation:

- The rate differential is significant. If the assumed rate is at least 1.5–2% lower than current mortgage rates, the monthly savings are likely worth the additional complexity.

- You can cover the equity gap. Either through cash reserves or secondary financing, you need a plan for the seller’s equity.

- You plan to stay in the home long-term. The longer you hold the loan, the more you benefit from the lower rate.

- The property has an FHA, VA, or USDA loan. Most assumable mortgage opportunities exist in these loan categories.

On the other hand, a new mortgage might be a better fit if the equity gap requires a large second loan that offsets the rate savings, or if you plan to move within a few years. Talking through both scenarios with a licensed loan officer helps you run the numbers for your specific situation.

If you’re comparing options, explore the Champions Mortgage conventional loan programs, refinance options, or use the mortgage calculator to model your monthly payment under different scenarios.

Common Mistakes When Assuming a Mortgage

- Skipping lender approval: Never assume a mortgage through a private arrangement. Always get formal lender sign-off and a written release of liability for the seller.

- Underestimating the equity gap: Calculate how much cash or secondary financing you’ll need before making an offer. Surprise equity shortfalls can kill a deal at closing.

- Ignoring the FHA MIP carry-over: On FHA assumptions, the annual mortgage insurance premium doesn’t go away. Factor it into your monthly cost comparison.

- Assuming VA entitlement automatically restores: If a non-veteran assumes a VA loan, the selling veteran’s entitlement stays tied to the property until the mortgage is paid off.

- Not shopping the second mortgage: If you need financing to cover the equity gap, shop multiple lenders for the best rate on the second loan — it can meaningfully affect your total cost.

Frequently Asked Questions: Assumable Mortgages

What types of mortgages are assumable?

FHA loans, VA loans, and USDA loans are generally assumable. Most conventional mortgages are not assumable because they include a due-on-sale clause that requires full repayment when the property changes hands. Some conventional adjustable-rate mortgages may be assumable, but this is uncommon.

Can a non-veteran assume a VA loan?

Yes. A buyer does not need to be a veteran or active-duty military member to assume a VA loan. However, if a non-veteran assumes the loan, the selling veteran’s VA entitlement remains tied to that mortgage until it is fully paid off, which can affect their ability to use VA benefits on a future home purchase.

What credit score do I need to assume a mortgage?

For FHA loan assumptions, most lenders require a minimum credit score of 580, with some requiring 620. VA and USDA assumptions do not have a federally mandated floor, but most lenders set a practical minimum in the 620–640 range. The lender will also review your debt-to-income ratio and income documentation.

How much can I save with an assumable mortgage loan?

Savings depend on the rate differential and loan balance. On a $260,000 assumed loan at 3.25% versus taking out a new loan at 6.75%, the monthly savings on principal and interest alone exceed $400 per month — more than $4,800 per year and potentially over $100,000 across the life of the remaining loan term.

What is a due-on-sale clause?

A due-on-sale clause is a provision in most conventional mortgage contracts that requires the borrower to repay the full loan balance when the property is sold or transferred. Government-backed loans — FHA, VA, and USDA — are exempt from this clause, which is why they can be assumed by a new buyer.

What are the closing costs on an assumable loan ?

Closing costs on assumable loans are typically lower than on new mortgages. Common costs include an assumption fee (varies by loan type), a VA funding fee of 0.5% for VA loans, USDA processing fees of $300–$500, and title transfer fees. You’ll also pay costs associated with any second mortgage taken out to cover the seller’s equity.

What happens to the seller after assumption?

With a formal, lender-approved assumption, the seller receives a release of liability and is no longer responsible for the mortgage. Without formal approval, the seller remains liable if the buyer defaults. For VA loan sellers, their entitlement stays tied to the property until payoff unless the buyer is also a veteran who can substitute their own entitlement.

How do I find assumable mortgage listings?

Ask your real estate agent to identify FHA, VA, and USDA-financed homes in your target market. Specialized platforms like AssumeList aggregate assumable listings. You can also ask sellers’ agents directly whether the existing loan is government-backed and assumable. Working with a lender experienced in mortgage assumptions will help you verify eligibility and move quickly.

Can I assume a USDA loan?

Yes, USDA loans are assumable. The buyer must meet the USDA’s income eligibility requirements — household income generally cannot exceed 115% of the area median income — and the property must remain in a USDA-eligible rural area. Processing fees typically run between $300 and $500.

The Bottom Line

An assumable mortgage is one of the most underutilized tools available to today’s homebuyers. In a mortgage market where rates are significantly higher than they were just a few years ago, the ability to step into a seller’s low-rate home loan can translate into real, lasting savings — sometimes hundreds of dollars per month for the remaining life of the loan.

The strategy isn’t without its complexities. The equity gap, lender approval requirements, MIP considerations, and potential impact on VA entitlement all require careful planning. But for buyers who qualify and find the right property, an assumable mortgage could be the smartest home financing decision available in today’s environment.

At Champions Mortgage Team, our loan officers have hands-on experience helping Texas buyers navigate FHA loan assumptions, VA loan assumptions, and a full range of home purchase strategies. Whether you’re exploring assumable loans or comparing other loan programs, we’re ready to help you find the financing that works for your goals.

| Ready to Explore Your Options? Talk to a Champions Mortgage loan officer today about assumable mortgages and whether one is right for your home purchase. Get Your Custom Rate → championsmortgageteam.com 📞 Call: (281) 727-2500 | ✉ info@championsmortgageteam.com |